Tiger Global SC Verdict: Why the Focus Has Shifted from Tax Residency Certificates to Investment Legitimacy

The Supreme Court’s landmark ruling on Tiger Global and Flipkart marks a paradigm shift in Indian tax law. Learn how the focus has moved from “documentary evidence” to “investment legitimacy” and what this means for PE/VC firms using tax-haven jurisdictions.

The landscape of cross-border investments in India underwent a seismic shift this Thursday. In a landmark judgment, the Supreme Court of India ruled that global investment giant Tiger Global is liable to pay capital gains tax on its high-profile 2018 exit from the e-commerce unicorn Flipkart.

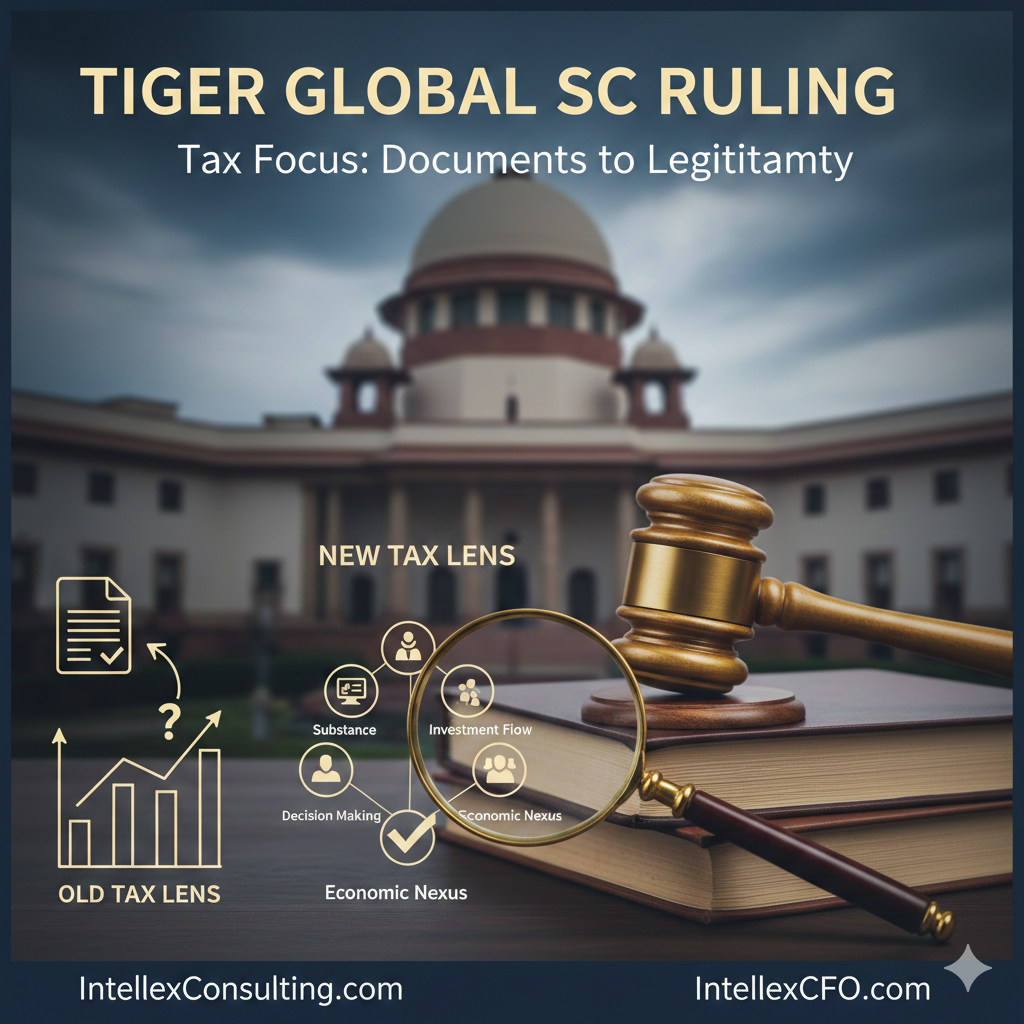

For decades, foreign investors relied on “Treaty Shopping” and the presentation of a Tax Residency Certificate (TRC) as a “golden ticket” to tax exemption. This ruling effectively tears up that script, signaling that the Indian tax lens has officially moved from mere documentation to the substance and legitimacy of the investment structure.

The Core of the Dispute: The 2018 Flipkart-Walmart Deal

The case dates back to one of the largest deals in the Indian startup ecosystem: Walmart’s acquisition of a majority stake in Flipkart. Tiger Global, through its Mauritius-based entities, sold its shares and claimed tax exemption under the Indo-Mauritius Double Taxation Avoidance Agreement (DTAA).

The Arguments

- Tiger Global’s Stand: The Mauritius entities held valid Tax Residency Certificates (TRCs). Per previous precedents (like the Azadi Bachao Andolan case), a TRC was considered sufficient evidence of residence to claim treaty benefits.

- The Revenue Department’s Stand: The tax authorities argued that the Mauritius entities were mere “conduit companies” with no real commercial substance. They alleged that the real control and management resided in the United States, making the structure a “colorable device” for tax avoidance.

From “Forms” to “Substance”: The Paradigm Shift

The Supreme Court’s decision marks a departure from the literal interpretation of tax treaties. The ruling emphasizes that while a TRC is a necessary document, it is not an insurmountable shield if the legitimacy of the investment is in question.

1. Piercing the Corporate Veil

The court highlighted that tax authorities have the right to look behind the curtain. If an entity is found to be a shell company created solely to route funds and bypass domestic tax laws, the benefits of the DTAA can be denied.

2. The “LOB” Principle (Limitation of Benefits)

While the older treaty versions were more relaxed, this ruling aligns with the modern global shift toward BEPS (Base Erosion and Profit Shifting) frameworks. It reinforces that “substance over form” is now the governing principle for Indian tax assessments.

3. Investment Legitimacy

The “Tax Lens” is no longer just checking if the paperwork is in order. It now examines:

- Where the key decisions are made (Place of Effective Management).

- Whether the entity has independent employees, office space, and local expenses.

- The flow of funds and whether the entity has “beneficial ownership” of the gains.

Impact on Past and Future Investments

This ruling sends ripples through the Private Equity (PE) and Venture Capital (VC) communities, particularly those who invested in Indian startups before the 2017 amendment to the Mauritius treaty.

|

Impact Area |

Consequences |

|---|---|

|

Legacy Investments |

Deals closed between 2017–2019 that relied on treaty benefits may now face renewed scrutiny and litigation. |

|

Due Diligence |

Investors will now require much more rigorous “substance” audits before entering or exiting the Indian market. |

|

Jurisdiction Choice |

The allure of Mauritius or Singapore may diminish if the “substance” requirements become too burdensome compared to direct investment. |

|

Valuations |

With a higher probability of capital gains tax (approx. 10–20% depending on the era/type), net exit proceeds for investors may shrink. |

The Road Ahead: A New Era of Tax Compliance

The Tiger Global verdict is a clear message from the Indian judiciary: Tax planning is permissible, but tax avoidance through artificial structures is not. For the Indian startup ecosystem, this might lead to more transparent funding rounds. However, it also raises concerns about “tax terrorism” or retrospective-style scrutiny that could dampen investor sentiment in the short term.

As India continues to tighten its regulatory grip through GAAR (General Anti-Avoidance Rules), global funds must ensure that their offshore offices are more than just “brass plate” entities. In the eyes of the Supreme Court, legitimacy is no longer on paper but it’s in the practice.

Team: IntellexCFO.com

More Featured Articles:

Top 10 Angel Investment Networks in India (2026): The Ultimate Founder’s Guide to Fundraising.

Startup Funding Stages Explained: How to Raise Capital from Pre-Seed to Pre-IPO

Hyderabad Angel Fund Launches Rs 100 Crore Fund to Support High-Potential Startups in India

Angrezi Dhaba Franchise Opportunities 2025: India’s Premium Fusion Dining Brand Expands Globally.

Expert Accounting & Taxation and Statutory Compliances Solutions across Indian Cities

Why MSMEs Trust Us With Their Most Critical Financial Decisions

.")

Companies in India.")

: A Complete Guide to Section 138.")